Many entrepreneurs believe that once they form an LLC, their personal credit no longer matters.

Then they apply for business funding — and get denied.

Here’s the truth most lenders won’t say out loud:

👉 In 2025, your personal credit still controls your business funding — until you deliberately break the link.

This article explains why personal credit matters so much, how lenders actually evaluate risk, and what steps business owners can take to unlock funding without being trapped by their personal credit forever.

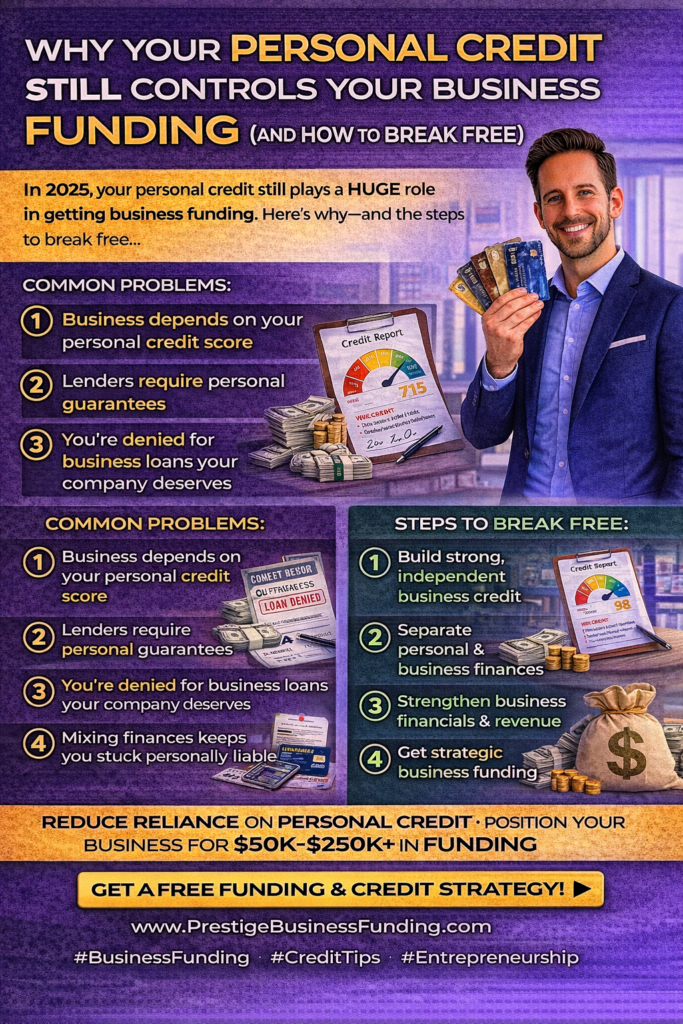

Why Business Owners Are Surprised by Funding Denials

Most small business owners do everything “right”:

- They form an LLC

- Open a business bank account

- Get an EIN

- Start generating revenue

Yet lenders still ask for:

- A personal credit check

- A personal guarantee

- The owner’s SSN

That’s not a mistake — it’s by design.

The Real Reason Personal Credit Still Matters

In 2025, lenders care about risk, not business dreams.

For most small businesses:

- Less than 2 years old

- Limited financial history

- Inconsistent cash flow

…the only proven repayment track record is the owner’s personal credit.

To lenders, your personal credit answers one key question:

“How has this person handled debt in the past?”

Until your business proves itself independently, you are the risk profile.

When Personal Credit Controls Business Funding

Personal credit typically controls funding when:

- Your business is under 24 months old

- You don’t have established business credit

- Your business revenue is inconsistent

- You lack strong business banking history

In these cases, lenders use personal credit as a substitute for missing data.

What Lenders Actually Look at (Not Just Your Score)

Many owners focus on their FICO score — but lenders evaluate much more.

They analyze:

- Credit utilization

- Payment history trends

- Recent inquiries

- Derogatory items (collections, charge-offs)

- Debt-to-income ratios

- Personal cash flow

A high score with poor structure can still result in denial.

The Difference Between “Good Credit” and “Fundable Credit”

This is where most people get stuck.

Good credit:

- Looks fine on paper

- May still trigger rejections

Fundable credit:

- Low utilization

- Clean recent history

- Strategic inquiry timing

- Strong payment patterns

Fundable credit gets approvals — even if the score isn’t perfect.

Why Personal Guarantees Are So Common

Lenders use personal guarantees because:

- They reduce lender risk

- They ensure accountability

- They increase approval odds

Until your business can stand on its own, lenders want reassurance — and that reassurance is you.

How to Break Free From Personal Credit Dependency

Breaking free doesn’t happen automatically. It’s a process.

Here’s how business owners do it successfully.

1️⃣ Build Business Credit the Right Way

Business credit must be:

- Properly structured

- Actively reported

- Separated from personal credit

This includes:

- Vendor accounts

- Net-30 tradelines

- Tiered credit progression

Without reporting, business credit doesn’t exist.

2️⃣ Strengthen Business Banking Behavior

Lenders closely review:

- Average daily balances

- Deposit consistency

- NSF and overdrafts

- Revenue stability

Clean bank statements reduce reliance on personal credit.

3️⃣ Establish Time in Business

Time matters.

As your business ages:

- Risk decreases

- Approval amounts increase

- Guarantee requirements soften

This is why many funding strategies are time-based, not instant.

4️⃣ Use Strategic Funding to Build Independence

Many business owners use early funding to:

- Build stronger cash flow

- Improve business financials

- Qualify for better funding later

The goal isn’t just approval — it’s progression.

5️⃣ Separate Finances Completely

This is critical.

To break free:

- No personal expenses on business accounts

- No business expenses on personal cards

- Clear owner compensation structure

Separation signals maturity and lowers lender risk.

When Business Credit Can Fully Stand Alone

In many cases, personal credit influence decreases when:

- Business is 2+ years old

- Revenue is stable

- Business credit profile is strong

- Banking history is clean

At this stage, some lenders approve funding without personal guarantees.

Common Mistakes That Keep Owners Stuck

Avoid these traps:

- Applying too early

- Ignoring business credit setup

- Overusing personal credit

- Mixing finances

- Chasing funding without preparation

These mistakes delay independence.

Final Thoughts

Your personal credit controls business funding until your business proves it doesn’t need to.

That’s not unfair — it’s how risk works.

The good news?

✔ You can reduce personal credit dependence

✔ You can build independent business funding power

✔ You can unlock larger approvals over time

But it requires strategy, structure, and patience.

Need Personal Or Business Funding? Prestige Business Financial Services LLC offer over 30 Personal and Business Funding options to include good and bad credit options. Get Personal Loans up to $100K or 0% Business Lines of Credit Up To $250K. Also Enhanced Credit Repair ($249 Per Month) and Passive income programs (Can Make 5-10% Per Month; Trade $100K of Someone Esles Money). Our 2nd Passive Income Program could make 1-2% Per Day Compounding ($500 to Start, In 2 years could be $6 Million).

Book A Free Consult And We Can Help - https://prestigebusinessfinancialservices.com

Email - anthony@prestigebfs.com

Phone- 1-800-622-0453

🚀 Call to Action

If you want to:

- Stop being denied for business funding

- Reduce reliance on personal credit

- Build true business credit

- Position your business for $50K–$250K+ in funding

Prestige Business Financial Services can help you create a step-by-step funding and credit strategy.

👉 Visit: www.prestigebusinessfinancialservices.com

👉 Or message “Break Free” for a free funding and credit evaluation

No comments:

Post a Comment