Applying for business funding can be the difference between growth and stagnation.

But here’s the reality:

👉 Many small business owners get denied—not because they don’t qualify, but because they make avoidable mistakes.

The good news?

✔ Once you understand these mistakes, you can position yourself for approval and better terms

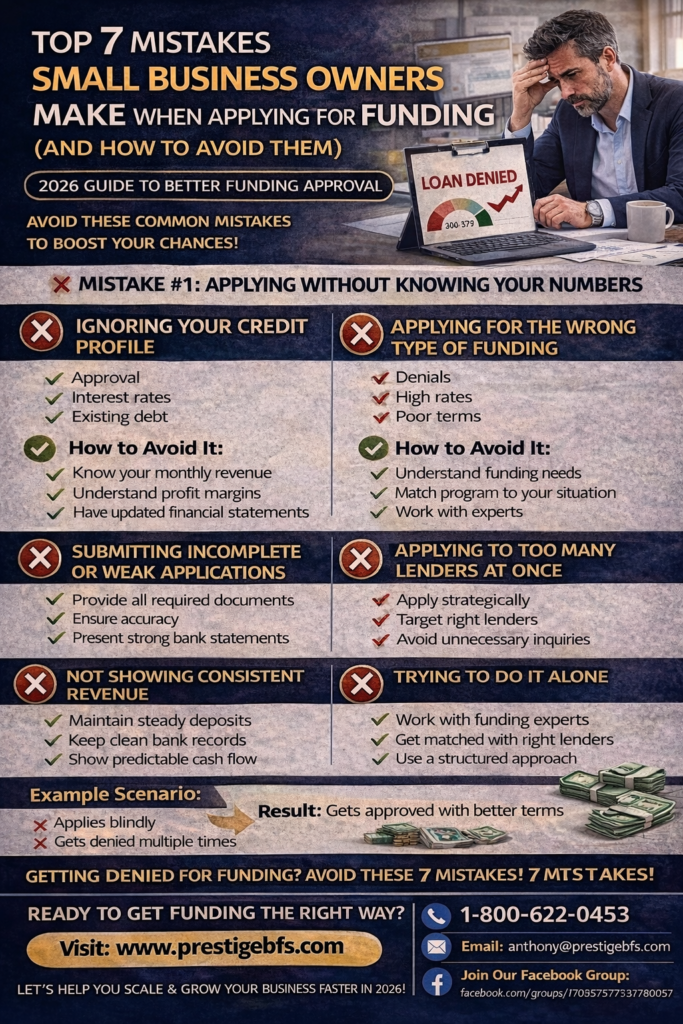

❌ Mistake #1: Applying Without Knowing Your Numbers

Many business owners apply for funding without understanding:

- Revenue

- Expenses

- Cash flow

- Existing debt

✅ How to Avoid It:

✔ Know your monthly revenue

✔ Understand your profit margins

✔ Have updated financial statements ready

👉 Lenders want to see that you understand your business financially.

❌ Mistake #2: Ignoring Your Credit Profile

Your credit plays a major role in:

✔ Approval

✔ Interest rates

✔ Loan terms

✅ How to Avoid It:

✔ Check your personal credit score

✔ Review your business credit (PAYDEX)

✔ Fix errors before applying

👉 Even small improvements can increase approval odds.

❌ Mistake #3: Applying for the Wrong Type of Funding

Not all funding is the same.

👉 Applying for the wrong product can lead to:

❌ Denials

❌ High rates

❌ Poor terms

✅ How to Avoid It:

✔ Understand your funding needs

✔ Match the right program to your situation

✔ Work with experts who know all options

❌ Mistake #4: Submitting Incomplete or Weak Applications

Incomplete applications are one of the top reasons for denial.

✅ How to Avoid It:

✔ Provide all required documents

✔ Ensure accuracy

✔ Present strong bank statements

👉 A strong application builds lender confidence.

❌ Mistake #5: Applying to Too Many Lenders at Once

This can:

❌ Hurt your credit score

❌ Make you look desperate

❌ Lower approval chances

✅ How to Avoid It:

✔ Apply strategically

✔ Target the right lenders first

✔ Avoid unnecessary inquiries

❌ Mistake #6: Not Showing Consistent Revenue

Lenders want stability.

If your revenue is inconsistent:

👉 It increases perceived risk

✅ How to Avoid It:

✔ Maintain steady deposits

✔ Keep clean bank records

✔ Show predictable cash flow

❌ Mistake #7: Trying to Do It Alone

Many business owners go directly to lenders without a strategy.

👉 This often leads to:

❌ Denials

❌ Poor terms

❌ Missed opportunities

✅ How to Avoid It:

✔ Work with funding experts

✔ Get matched with the right lenders

✔ Use a structured approach

📊 Example Scenario

Business Owner A:

- Applies blindly

- Gets denied multiple times

Business Owner B:

- Prepares financials

- Targets the right funding

- Works with experts

👉 Result: Gets approved with better terms

🚨 Quick Recap

Avoid these 7 mistakes:

- Not knowing your numbers

- Ignoring credit

- Choosing wrong funding

- Weak application

- Too many applications

- Inconsistent revenue

- Doing it alone

💡 Final Thoughts

Getting approved for funding isn’t just about applying—it’s about strategy.

Small business owners who prepare properly can:

✔ Increase approval odds

✔ Secure better rates

✔ Access more capital

👉 The right approach makes all the difference

📈 2026 Trending Keywords (SEO Placement)

- business funding mistakes

- why business loans get denied

- how to get approved for business funding

- small business loan tips 2026

- funding strategies for entrepreneurs

🚀 Call to Action

If you’re ready to:

✔ Avoid costly funding mistakes

✔ Get approved faster

✔ Access the best funding programs

👉 Visit: https://prestigebfs.com

📞 Call: 1-800-622-0453

📧 Email: anthony@prestigebfs.com

👉 Join our Facebook Group for funding tips, strategies, and opportunities:

https://www.facebook.com/groups/1703575773378057

Let’s help you get the funding your business deserves 🚀

No comments:

Post a Comment