Many people proudly say, “I have good credit.”

Yet when they apply for funding, they’re shocked to receive a denial or a much smaller approval than expected.

👉 Here’s the truth: good credit is not the same as fundable credit.

In 2025, lenders don’t just approve based on scores — they approve based on structure, behavior, and risk signals. This misunderstanding is one of the biggest reasons small business owners miss out on $25K–$250K+ in funding.

This article breaks down the real difference between good credit and fundable credit — and how to position yourself so lenders say yes.

What Is “Good Credit”?

Good credit is usually defined by a score.

Typically:

- 680–720+ FICO score

- On-time payment history

- No recent major derogatory events

Good credit looks nice on paper — but it doesn’t tell lenders how risky you are today.

Why Good Credit Alone Doesn’t Guarantee Funding

In 2025, lenders use advanced underwriting models that analyze more than just your score.

They evaluate:

- Credit utilization trends

- Recent inquiries

- Account behavior

- Debt-to-income ratios

- Banking activity

- Timing of applications

You can have a 720 score and still look high risk.

What Is Fundable Credit?

Fundable credit is credit that is structured, optimized, and positioned for approvals.

It answers the lender’s real question:

“Can we safely lend this person a large amount of money right now?”

Fundable credit focuses on how your credit behaves, not just how it scores.

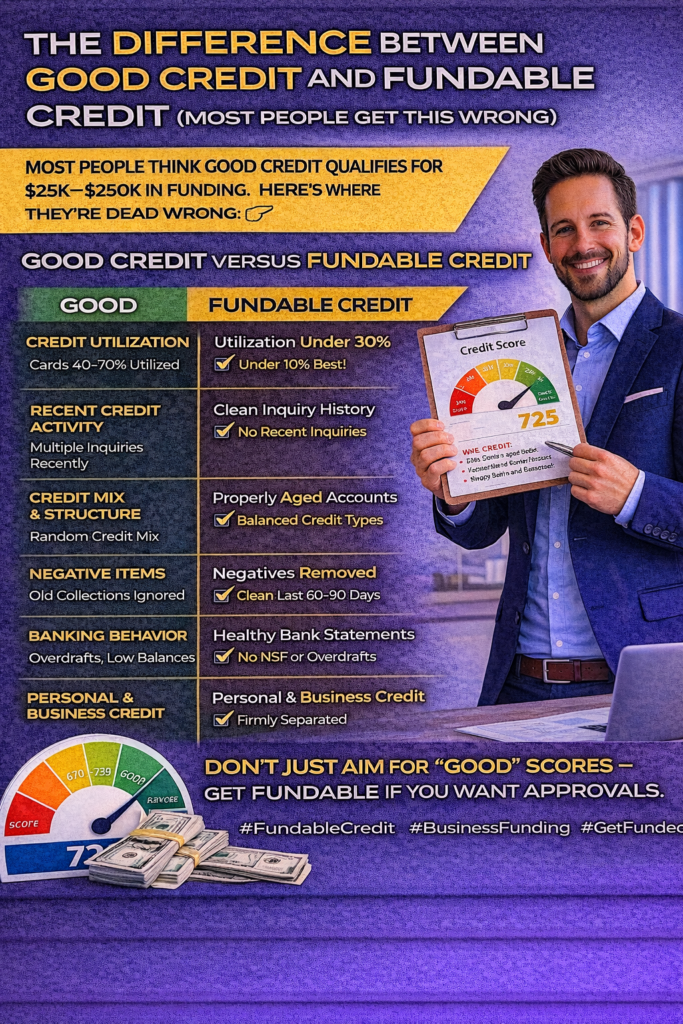

🔍 Key Differences Between Good Credit and Fundable Credit

1️⃣ Credit Utilization

Good credit:

- Cards may be 40–70% utilized

Fundable credit:

- Utilization under 30%

- Under 10% for top-tier approvals

📌 High balances are one of the fastest ways to lose funding power.

2️⃣ Recent Credit Activity

Good credit:

- Multiple recent applications

- Several hard inquiries

Fundable credit:

- Clean inquiry history

- Strategic, well-timed applications

Lenders prefer patience and planning over urgency.

3️⃣ Credit Mix & Structure

Good credit:

- Random mix of cards and loans

Fundable credit:

- Properly aged accounts

- Balanced revolving and installment credit

- Limits that support low utilization

Structure matters as much as score.

4️⃣ Negative Items

Good credit:

- Old collections or charge-offs ignored

Fundable credit:

- High-impact negatives addressed or removed

- Clean recent history (last 60–90 days)

Recent behavior outweighs old mistakes.

5️⃣ Banking Behavior

Good credit:

- Bank overdrafts

- Low average balances

Fundable credit:

- Clean bank statements

- Consistent deposits

- No NSF or overdraft fees

Credit and banking work together.

6️⃣ Personal vs Business Credit

Good credit:

- Personal credit only

Fundable credit:

- Personal credit optimized

- Business credit established

- Separation of finances

This is how entrepreneurs unlock six-figure funding.

Why Lenders Care About Fundable Credit

Lenders are not emotional — they are statistical.

Fundable credit signals:

✔ Stability

✔ Predictability

✔ Lower default risk

✔ Strong repayment likelihood

Good credit without structure still looks risky.

How to Turn Good Credit Into Fundable Credit

✅ Optimize utilization before applying

✅ Pause applications for 60–90 days

✅ Clean up recent negatives

✅ Improve bank statement behavior

✅ Build and report business credit

✅ Apply with a strategy — not desperation

Most people don’t need better credit — they need better positioning.

What a Fundable Credit Profile Looks Like

Borrowers who get approved consistently show:

- Low utilization

- Minimal recent inquiries

- Clean recent payment history

- Strong banking activity

- Business credit in place

- Strategic application timing

This profile unlocks larger limits, better terms, and repeatable funding.

Final Thoughts

Good credit helps you sleep at night.

Fundable credit helps you get approved.

If lenders keep saying no, the problem usually isn’t your score — it’s your credit structure.

Once you shift from “good” to fundable, funding becomes predictable instead of frustrating.

Need Personal Or Business Funding? Prestige Business Financial Services LLC offer over 30 Personal and Business Funding options to include good and bad credit options. Get Personal Loans up to $100K or 0% Business Lines of Credit Up To $250K. Also Enhanced Credit Repair ($249 Per Month) and Passive income programs (Can Make 5-10% Per Month; Trade $100K of Someone Esles Money). Our 2nd Passive Income Program could make 1-2% Per Day Compounding ($500 to Start, In 2 years could be $6 Million).

Book A Free Consult And We Can Help - https://prestigebusinessfinancialservices.com

Email - anthony@prestigebfs.com

Phone- 1-800-622-0453

🚀 Call to Action

If you want to:

- Turn your credit into a fundable profile

- Qualify for personal or business funding

- Unlock $25K–$250K+ in approvals

- Stop guessing and start getting approved

Prestige Business Financial Services can help.

👉 Visit: www.prestigebusinessfinancialservices.com

👉 Or message “Fundable Credit” for a free credit and funding evaluation

No comments:

Post a Comment