Credit repair has changed dramatically in the last few years.

Strategies that worked in 2018 or even 2022 often don’t work anymore — and some can actually hurt your score in 2025.

👉 The truth is this: credit repair still works, but only when it’s done strategically, legally, and in alignment with how modern lenders and credit bureaus evaluate risk.

This guide breaks down:

- What actually works in credit repair in 2025

- What no longer works (and why)

- How people are still boosting 100+ points faster than ever

Why Credit Repair Looks Different in 2025

Credit bureaus and lenders now use:

- AI-driven risk models

- Behavior-based scoring

- Trend analysis over time

- Real-time data updates

That means disputing everything blindly or waiting years for items to “fall off” is no longer effective.

Credit repair in 2025 is about structure, timing, and behavior — not shortcuts.

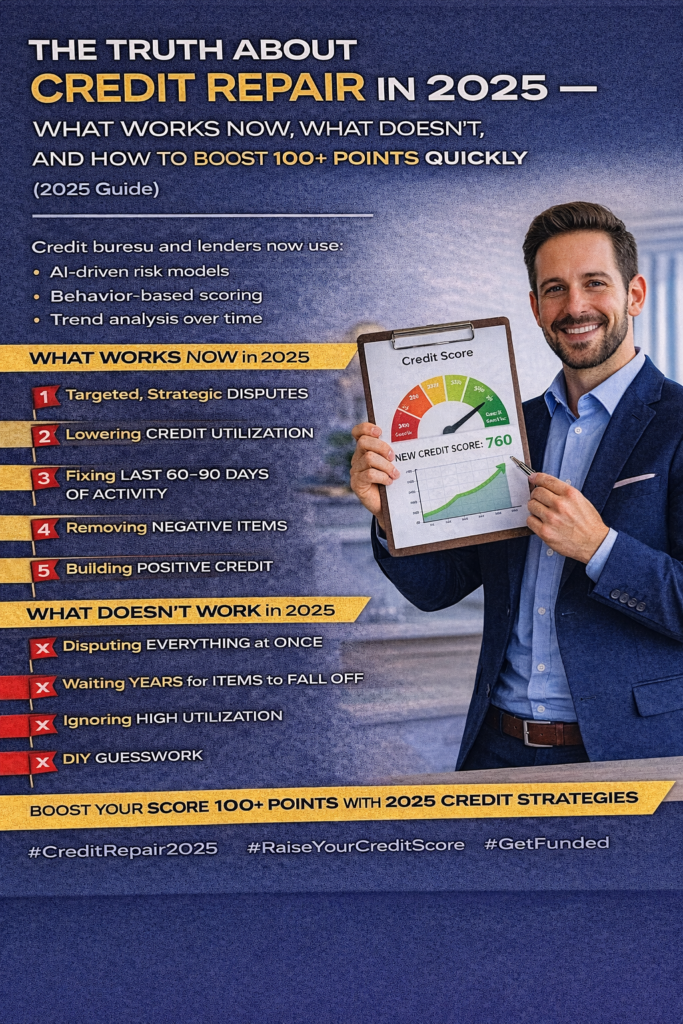

✅ What ACTUALLY Works in Credit Repair in 2025

1️⃣ Targeted, Strategic Disputes (Not Mass Disputes)

Random disputes no longer move the needle.

What works now:

- Disputing inaccurate, outdated, or unverifiable data

- Using correct legal language

- Targeting items that impact utilization, payment history, and recent activity

📌 Strategic disputes outperform mass disputes every time.

2️⃣ Lowering Credit Utilization (Fastest Point Gains)

This is still the #1 fastest way to increase your score.

In 2025:

- Under 30% utilization = strong improvement

- Under 10% utilization = maximum scoring benefit

Many people see 20–60 points increase just from lowering balances.

3️⃣ Fixing the Last 60–90 Days of Activity

Lenders care most about recent behavior.

What works:

- Eliminating late payments

- Preventing new collections

- Stabilizing balances

- Avoiding new inquiries

A clean recent history can outweigh older negative items.

4️⃣ Removing or Settling High-Impact Negatives

Not all negative items are equal.

High-impact items include:

- Collections

- Charge-offs

- Repos

- Recent late payments

When handled correctly, removing or resolving these can unlock massive point increases.

5️⃣ Building Positive Credit While Repairing

Credit repair alone is not enough.

What works best in 2025:

- Adding positive tradelines

- Opening the right type of accounts

- Building business credit alongside personal credit

This speeds recovery and strengthens your overall profile.

❌ What NO LONGER Works in Credit Repair

🚫 Disputing Everything at Once

Triggers bureau resistance and slows results.

🚫 Credit “Sweeps” or Fake Identities

Illegal and dangerous — often leads to freezes or investigations.

🚫 Waiting Years for Items to Fall Off

Costs opportunities, funding, and approvals.

🚫 Ignoring Utilization

You can’t dispute high balances away.

🚫 DIY Guesswork

One wrong move can drop your score instead of raising it.

🚀 How People Are Boosting 100+ Points in 2025

The biggest score jumps come from combining strategies, not relying on one fix.

Typical 100+ point improvements involve:

- Lowering utilization

- Removing 1–3 high-impact negatives

- Cleaning recent activity

- Adding positive credit

- Improving banking behavior

📌 Credit repair works fastest when it’s paired with a funding and credit-building strategy, not just disputes.

How Long Does Credit Repair Take in 2025?

While every profile is different, many people see:

- Initial improvements in 30–45 days

- Significant gains in 60–90 days

- Strong funding-ready profiles in 90–120 days

Speed depends on how proactive and strategic the plan is.

Final Thoughts

Credit repair in 2025 isn’t about tricks — it’s about understanding the system.

When done correctly:

✔ Scores increase faster

✔ Approvals improve

✔ Interest rates drop

✔ Funding becomes accessible

You don’t need perfect credit — you need proper positioning.

Need Personal Or Business Funding? Prestige Business Financial Services LLC offer over 30 Personal and Business Funding options to include good and bad credit options. Get Personal Loans up to $100K or 0% Business Lines of Credit Up To $250K. Also Enhanced Credit Repair ($249 Per Month) and Passive income programs (Can Make 5-10% Per Month; Trade $100K of Someone Esles Money). Our 2nd Passive Income Program could make 1-2% Per Day Compounding ($500 to Start, In 2 years could be $6 Million).

Book A Free Consult And We Can Help - https://prestigebusinessfinancialservices.com

Email - anthony@prestigebfs.com

Phone- 1-800-622-0453

🚀 Call to Action

If you want to:

- Raise your credit score fast

- Remove negative items legally

- Build credit the right way

- Qualify for personal or business funding

Prestige Business Financial Services can help.

👉 Visit: www.prestigebusinessfinancialservices.com

👉 Or message us “Credit Help” for a free credit evaluation

Even a strong score gets denied with high utilization.

Even a strong score gets denied with high utilization. Funding becomes predictable

Funding becomes predictable